How to Draft M&A Definitive Agreements

How to Draft M&A Definitive Agreements

When finalizing a business acquisition or sale, the definitive agreement is the legally binding document that cements every negotiated term. It’s not just about the purchase price - it outlines the deal structure, risk allocation, and compliance steps, especially in regulated industries like iGaming, Fintech, and Cryptocurrency. Here’s what you need to know:

- Purpose: It formalizes terms, manages risks, and ensures regulatory compliance.

- Key Components:

- Deal Description: Clearly defines what’s being sold (assets, stock, or entire company) and the price structure.

- Representations & Warranties: Seller’s factual assurances about the business, extending to financials, compliance, and licensing.

- Indemnification: Defines how post-closing risks and liabilities are handled, including caps, baskets, and survival periods.

- Regulated Industries: Agreements must address licensing, regulatory approvals, and compliance milestones specific to each jurisdiction.

- Payment Terms: Includes cash, seller notes, or earnouts tied to performance, with mechanisms like escrow or holdbacks for risk management.

Drafting these agreements requires precision, especially for regulated sectors, where compliance missteps can delay or derail deals. Whether it’s transferring licenses, meeting anti-money laundering standards, or securing regulatory approvals, every detail matters.

Let’s break it down further.

Definitive Agreement - Mergers & Acquisitions

Core Components of a Definitive Agreement

::: @figure  {M&A Definitive Agreement Indemnification Provisions: Market Standards and Thresholds}

{M&A Definitive Agreement Indemnification Provisions: Market Standards and Thresholds}

A definitive agreement rests on three main pillars: a precise description of the deal, factual assurances about the business, and a plan for resolving any post-closing disputes. Each element is designed to safeguard both parties and ensure the transaction concludes without unnecessary complications. Let’s break down these critical components.

Deal Description and Transaction Structure

The agreement must clearly outline what’s being sold - whether it’s specific assets, stock, or an entire company - and the structure of the transaction.

- In an asset purchase, the buyer cherry-picks assets and liabilities, leaving behind any unwanted obligations.

- A stock purchase involves acquiring the entire legal entity, including all historical liabilities - both known and unknown.

- A merger combines two entities into one new organization [4].

The purchase price should also be detailed, including any combination of cash, seller notes, stock, and earnout provisions tied to future performance [4][6].

To avoid disputes over working capital, the agreement should specify a "target working capital", often calculated as a 12-month average. This helps prevent unexpected price changes, which can swing by 5% to 15% post-closing [6]. Additionally, the agreement should clarify whether the transaction uses a locked box mechanism (fixing the price based on a historical balance sheet) or completion accounts (adjusting the price after closing based on actual financials at the closing date) [5].

Representations and Warranties

These are factual statements from the seller about the business, confirming its condition. They typically address areas such as financial accuracy, legal compliance, tax status, and asset ownership. For regulated industries, these assurances extend to licensing and compliance [4][5].

Representations and warranties are generally divided into three categories:

- Fundamental representations: Cover basics like the seller’s authority to sell and clear title to the assets.

- Regulatory or intermediate representations: Address specific issues like tax compliance, environmental matters, and licensing.

- Non-fundamental representations: Focus on operational details, such as customer contracts and inventory [7].

In highly regulated industries, buyers often push for "flat" representations - statements without qualifiers like "to the seller's knowledge" - to ensure the seller assumes full responsibility for any unknown issues. Alex Lubyansky, Managing Partner at Acquisition Stars, advises:

"Buyers should push for flat representations without knowledge qualifiers on critical items like litigation, tax compliance, and financial accuracy." [6]

Sellers, on the other hand, should prepare detailed disclosure schedules outlining any exceptions to these representations, as these documents are essential for avoiding post-closing disputes [8].

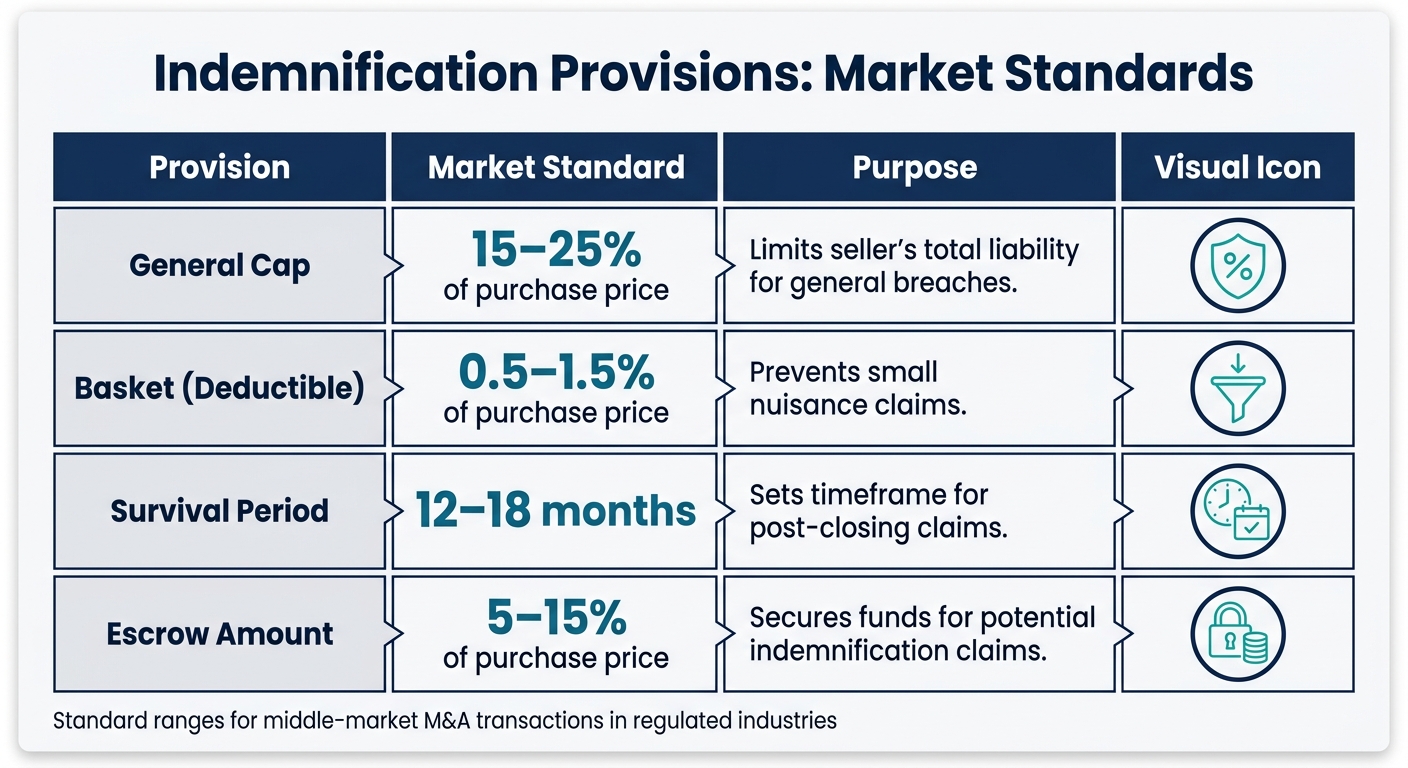

Indemnification and Risk Allocation

Indemnification provisions determine how risks and liabilities are addressed after closing. These typically include:

- Basket (or deductible): Sets a threshold - usually 0.5% to 1.5% of the purchase price - below which no claims can be made [6].

- Cap: Limits the seller’s total liability, with standard caps ranging from 15% to 25% of the purchase price for general breaches [6].

- Survival periods: Define how long the buyer has to make claims. General representations often survive for 12 to 18 months, while fundamental or tax-related matters may extend to three to six years [6][8].

In regulated industries, these provisions take on added importance due to the potential for compliance-related liabilities.

Buyers often require an escrow holdback, where 5% to 15% of the purchase price is held by a third party for 12 to 18 months to cover potential claims [6]. Alternatively, some deals rely on Warranty and Indemnity (W&I) insurance, which transfers risk to an insurer. With W&I insurance, sellers can often receive nearly all proceeds at closing, and indemnity caps may drop to just 0.5% to 1.5% of the purchase price [8].

| Provision | Market Standard | Purpose |

|---|---|---|

| General Cap | 15–25% of price | Limits seller’s total liability for general breaches |

| Basket (Deductible) | 0.5–1.5% of price | Prevents small nuisance claims |

| Survival Period | 12–18 months | Sets the timeframe for post-closing claims |

| Escrow Amount | 5–15% of price | Secures funds for potential indemnification claims |

Drafting for Regulated Industries

When drafting M&A agreements for industries like Fintech, iGaming, Cryptocurrency, or Forex, using standard commercial language simply won't cut it. These sectors operate under strict regulatory frameworks, which can lead to delays, higher transaction costs, or even failed deals if not addressed properly. To avoid these pitfalls, agreements must cover key areas such as license transferability, regulatory approval timelines, and compliance representations that go well beyond standard commercial transactions.

License Transfers and Regulatory Approvals

The choice between a stock purchase and an asset purchase directly impacts the regulatory process. In a stock acquisition, the licensed entity remains intact, but any change in ownership triggers "change of control" approvals. These approvals require regulators to vet the new owners. On the other hand, an asset acquisition typically requires the buyer to apply for entirely new licenses, as licenses are often non-transferable. This can lead to operational disruptions [2].

To mitigate these risks, include closing conditions that require all regulatory approvals to be secured before the deal is finalized. For iGaming transactions, this often involves approvals from authorities like the Nevada Gaming Control Board or the New Jersey Division of Gaming Enforcement. Timelines for these approvals vary widely. For instance, Pennsylvania approvals generally take 3 to 6 months for applicants with clean records, while Nevada’s two-step process can take significantly longer [2].

The agreement should also define "control" in precise terms, tailored to the statutes of each jurisdiction.

"A buyer who approaches a gaming acquisition using the same diligence and structuring framework applied to a standard commercial transaction will encounter regulatory obstacles that are capable of delaying closing, increasing transaction cost, and, in the worst case, threatening the viability of the deal." – Acquisition Stars [2]

Since regulatory reviews can stretch over several months, it’s critical to include interim covenants to maintain operational and compliance standards before closing. These covenants ensure that the seller doesn’t make any changes to compliance protocols or operations that could jeopardize regulatory approval [2]. If management changes are anticipated, the agreement should allow for a transition period to complete key employee licensing processes before new management takes over [2].

For iGaming businesses, technical certifications also demand attention. Sellers should represent compliance with standards like GLI-19 (Interactive Gaming Systems) or GLI-33 (Sports Wagering Systems). If the buyer plans to migrate the target's platform to a new technology stack post-closing, the agreement should include a 3- to 6-month recertification timeline as part of the integration plan [2].

These licensing considerations naturally tie into compliance, requiring detailed representations and covenants.

Compliance Representations and Covenants

Beyond licensing, robust compliance representations are essential to ensure adherence to financial and operational regulations. In regulated industries like Fintech, iGaming, and Cryptocurrency, these representations must go beyond standard warranties. For example, compliance with the Bank Secrecy Act (BSA) is critical, especially regarding Title 31 requirements [2].

Under the BSA, entities in these industries may be classified as financial institutions. This requires them to file Currency Transaction Reports (CTRCs) for transactions exceeding $10,000 in a single gaming day, as well as Suspicious Activity Reports (SARs) for transactions over $5,000 that appear to involve illegal activity [2]. The agreement should confirm the seller’s compliance with these reporting obligations.

For businesses operating as Money Services Businesses (MSBs), the agreement must verify active registration with FinCEN and compliance with Customer Due Diligence (CDD) rules [2]. In iGaming deals, include covenants requiring enforcement of state self-exclusion lists and adherence to National Council on Problem Gambling (NCPG) standards [2].

Enhanced representations regarding the "suitability" of principals are also crucial. These often involve detailed requirements, such as 10-year personal histories, criminal background checks, and full disclosure of funding sources. Instead of relying on qualifiers like "to the seller’s knowledge", buyers should demand flat representations, holding the seller fully accountable for any undisclosed issues.

For multi-jurisdictional deals, the Multi-Jurisdictional Personal History Disclosure Form can streamline the licensing process when principals need approval across multiple states. Platforms like MyReadyMade can also assist with license transfers in over 50 jurisdictions, reducing administrative burdens [2].

Negotiating Payment and Consideration Terms

Once compliance and licensing are addressed, the next big step is structuring how the payment for the business will work. In industries like iGaming and Fintech, the way payments are structured - whether through cash, equity, or contingent payments - has a direct impact on how risks are shared between the buyer and seller. This structure can also play a significant role in how smoothly the deal closes. For regulated transactions, the allocation of risk is especially critical because it can affect compliance and timelines.

Forms of Consideration

Cash is the most straightforward and frequently used payment method, offering sellers immediate access to funds. However, in larger deals or situations where buyers need to conserve cash, alternative structures come into play. One such option is seller notes, where the buyer pays part of the purchase price over time through a promissory note secured by the business assets. This setup essentially makes the seller a lender, which carries some risk if the buyer faces financial trouble after the deal closes [12][4].

Earnouts are another option, linking payments to the business's performance after the sale. These are particularly useful in bridging valuation disagreements. In tech-driven sectors, sellers are often better off negotiating for revenue-based earnouts rather than those tied to EBITDA. Alex Lubyansky, Managing Partner at Acquisition Stars, explains:

"If you're the seller, push for revenue-based earnouts over EBITDA-based ones. EBITDA is easier for the buyer to manipulate by increasing expenses, changing accounting allocations, or loading corporate overhead" [6].

When drafting earnout agreements, it’s essential to include operating covenants that protect the metrics used to calculate the earnout. For example, in iGaming transactions, timelines for technical certifications should be factored in [2].

Additionally, it’s wise to set a target working capital, with a detailed calculation completed 60–90 days after the closing date [6].

Once the payment structure is in place, the next focus is on minimizing risks after the deal closes.

Escrow and Holdback Mechanisms

To manage post-closing risks, buyers often set aside a portion of the purchase price - typically 5–15% - in an escrow account or as a holdback. This reserve acts as a safeguard against potential claims, such as breaches of representations and warranties, undisclosed liabilities, or regulatory issues.

There’s a key difference between escrows and holdbacks. Escrow funds are held by a neutral third party, like a bank, while holdback funds remain with the buyer. Sellers generally prefer escrow accounts because they ensure the funds are set aside and are not subject to the buyer’s financial issues or disputes [10][11]. Buyers, on the other hand, may prefer a single escrow account to consolidate all funds for potential claims. Sellers might push for separate accounts to allow for earlier release of funds that are not in dispute [10].

In regulated industries, these mechanisms also address potential liabilities tied to compliance. For example, in iGaming and Fintech, part of the escrow should cover risks like Anti-Money Laundering (AML) violations under Title 31, failures in responsible gaming programs, or undisclosed Suspicious Activity Reports (SARs) [6][2].

The escrow agreement should clearly outline how funds are released. Joint Written Instructions (JWI), which require both parties’ consent before funds are disbursed, are often the preferred method [9]. Sellers may also negotiate for staged releases - for instance, releasing 50% of the escrow after six months if no claims have been made. This approach helps sellers regain access to funds sooner and encourages quicker resolution of any issues [6][11]. Escrow terms typically last 12–18 months but can extend to 24 months to align with the survival period for general representations and warranties [6][11][4].

To avoid delays, start the Know Your Customer (KYC) process with the escrow agent several days before closing. It’s also important to clarify how the escrow interacts with Representations and Warranty Insurance (RWI) - specifically, whether the buyer must exhaust insurance coverage before tapping into escrow funds [9][11].

Finalizing and Executing the Agreement

Finalizing and executing an agreement is the step where the binding terms of a transaction become official. This phase demands close collaboration between legal teams, stakeholders, and regulatory bodies to ensure every detail is in order. In tightly regulated industries like iGaming and Fintech, even small errors can derail a deal or lead to expensive disputes after closing.

Review and Approval Processes

Before signing, conduct a thorough internal review. Check that critical terms like "Adjusted EBITDA", "Net Working Capital", and "Material Adverse Effect" are clearly defined. Representations and warranties should include proper qualifiers, such as "to the best of Seller's knowledge", and meet agreed-upon materiality standards. It’s also crucial to confirm that the transaction structure - whether an asset sale, stock sale, or merger - is accurately outlined, as this determines which assets and liabilities transfer.

Next, confirm that all regulatory conditions are addressed. For example, ensure that all required approvals, such as those under the Hart-Scott-Rodino (HSR) Act, are listed as closing conditions. The HSR Act typically requires a 30-day waiting period (or 15 days for cash tender offers) before closing [13]. Depending on the transaction, approvals related to CFIUS or export controls may also be necessary. Additionally, review the covenants to separate pre-closing requirements - like maintaining ordinary business operations - from post-closing obligations, such as non-compete clauses or employee retention agreements.

The termination section should clearly outline the conditions under which the deal can be canceled and specify any break-up fees, which are often 2–3% of the Equity Purchase Price [1]. As Jacob Orosz, President of Morgan & Westfield, explains:

"The purchase agreement details the final terms of an acquisition, so understanding its features is critical to a successful M&A transaction." [4]

Execution and Closing Deliverables

After the agreement is fully reviewed, move to execution and prepare all closing deliverables. The buyer's legal team should create a closing checklist that includes every required document, ancillary agreement, and regulatory approval. This checklist acts as a guide for managing signatures and tracking the exchange of documents.

For more complex deals, a staggered sign-and-close structure may be beneficial. This approach allows for an interim period between signing the agreement and finalizing the closing. During this time, pre-closing conditions - like obtaining third-party consents or regulatory approvals - can be addressed. The seller must continue operating in the ordinary course of business during this period to avoid jeopardizing the transaction.

Identify any anti-assignment provisions or change-of-control clauses in contracts or licenses early on. These clauses often require third-party notification or consent, which is especially important for maintaining gaming licenses or payment processing agreements in regulated industries. Typically, the seller handles consents for existing contracts, while the buyer applies for any new licenses or permits needed after closing.

Before the closing date, conduct jurisdictional searches to confirm that assets or shares are free of encumbrances. If liens are discovered, obtain payout statements from creditors in advance so debts can be settled directly from the closing funds. Additionally, ensure that all ancillary documents - such as the Bill of Sale, Employment Agreements, Corporate Resolutions, and Escrow Agreements - are finalized and attached to the agreement.

On the day of closing, assemble a team to oversee document signings, which may include virtual closings or escrow releases to streamline the process. Confirm that all signatories are authorized, and once signatures are collected and funds are transferred, promptly complete state filings and secure any outstanding third-party consents to avoid legal complications.

Conclusion

Drafting definitive agreements in regulated industries requires an intense focus on detail, a solid grasp of regulatory frameworks, and carefully thought-out risk management. Unlike standard commercial deals, these agreements must address every element - such as representations, warranties, and indemnification clauses - with an eye on jurisdiction-specific compliance rules and complex licensing requirements. These elements act as a guide to crafting an agreement that can smoothly navigate regulatory challenges.

Interestingly, about 30% of middle-market M&A transactions encounter post-closing disputes [3], often due to insufficient regulatory planning. In regulated industries, certain ownership thresholds can activate significant compliance obligations. These must be explicitly addressed to avoid operational disruptions or breaches of regulatory requirements. Be sure to outline all regulatory milestones and compliance standards as part of the closing conditions. Additionally, include technical recertification timelines - typically spanning 3 to 6 months - in post-closing strategies [2].

FAQs

What’s the best deal structure for licensing - asset sale or stock sale?

The right deal structure hinges on the details of the transaction. Asset sales allow buyers to pick specific assets and liabilities, steer clear of hidden risks, and potentially enjoy tax benefits. This approach can also streamline licensing in industries with strict regulations. On the other hand, stock sales transfer ownership of the entire company, including its licenses, which can be a smoother option if those licenses cannot be transferred separately. It's crucial to weigh regulatory, tax, and licensing considerations when deciding on the most suitable structure.

Which reps and warranties matter most in regulated industries?

In industries like gaming, iGaming, and fintech, where regulations are strict, certain representations and warranties take center stage. The focus is on compliance with industry-specific laws, cybersecurity, and data privacy. Critical areas include meeting both state and federal regulatory requirements, maintaining technical certifications, adhering to anti-money laundering rules, and implementing robust data protection practices. These elements are essential for gaining regulatory approval, reducing risks, and ensuring operations run smoothly in these high-stakes fields.

When should I use escrow vs RWI insurance?

Escrow and RWI (Reps and Warranties Insurance) play distinct roles in M&A transactions. Escrow involves setting aside a portion of the purchase price in a neutral third-party account. This fund acts as a safeguard, covering potential post-closing claims such as breaches of representations or indemnities.

RWI insurance, however, shifts those risks to an insurer. By doing so, it often reduces or even eliminates the need for escrow, allowing sellers to access more of the purchase price upfront and increasing liquidity.

The decision between these options typically hinges on factors like the size of the transaction, the parties' risk tolerance, and their individual preferences.

Related Articles

Ultimate Guide to Earnout Negotiations in M&A

Structure and negotiate earnouts in regulated M&A with clear metrics, anti-manipulation covenants, and acceleration or escrow protections.

How IP Affects Tokenization Valuation

How tokenizing patents, copyrights, and trademarks adds liquidity and market value—plus legal, regulatory, and valuation steps.

Regulatory Contingencies in M&A: What to Know

Anticipate regulatory approvals, antitrust and licensing risks in M&A—timelines, remedies, and contract protections.

Looking to Buy or Sell?

Get in touch with our team for personalized assistance