KYC vs. AML for Payment Processors: What to Know

KYC vs. AML for Payment Processors: What to Know

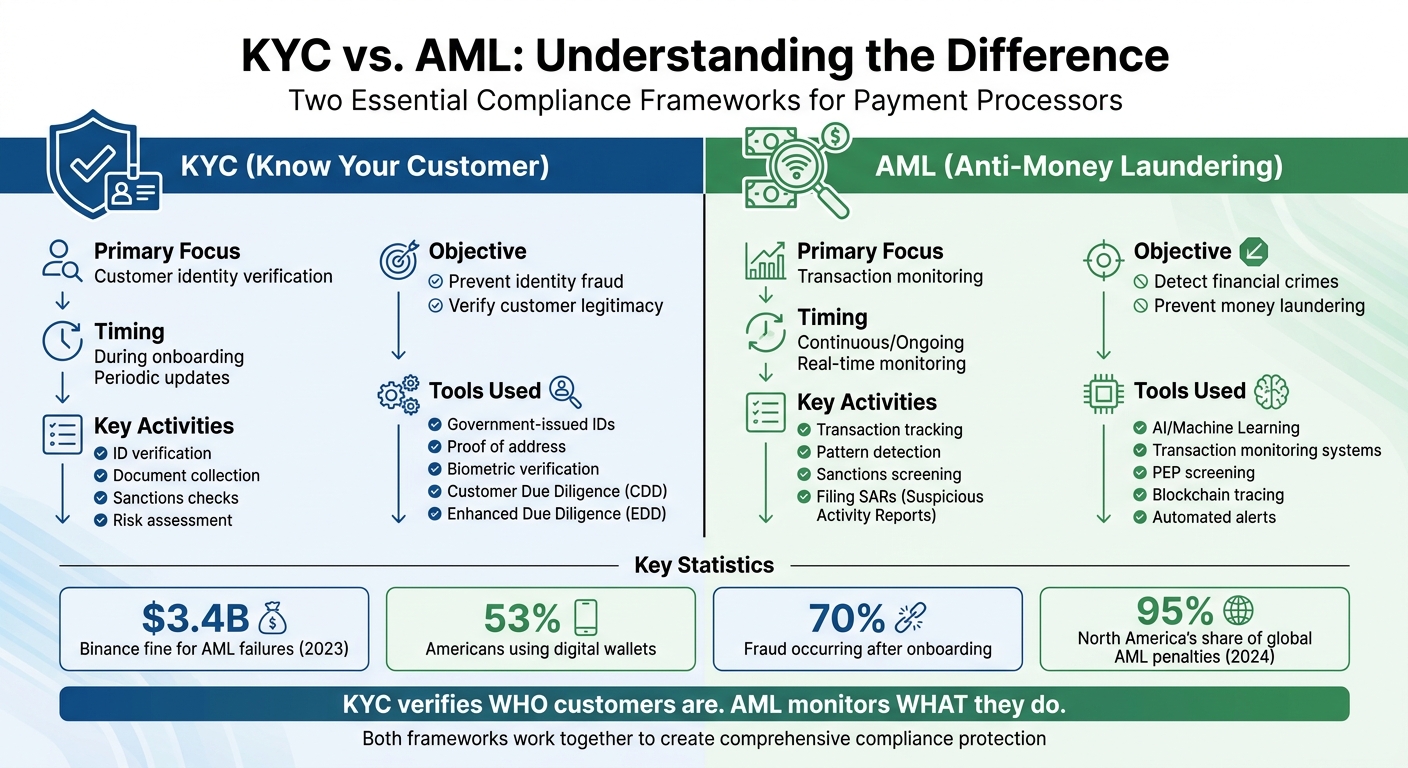

KYC (Know Your Customer) and AML (Anti-Money Laundering) are essential for payment processors to prevent financial crimes like money laundering, fraud, and sanctions violations. Here's the difference:

- KYC: Verifies customer identity during onboarding. It focuses on collecting and confirming personal or business details like IDs, proof of address, and ownership information.

- AML: Monitors transactions continuously to detect suspicious activities. It involves transaction tracking, sanctions screening, and filing suspicious activity reports (SARs).

Both work together to protect payment processors from regulatory fines, criminal liability, and reputational harm. For example, in 2023, Binance paid a $3.4 billion fine for AML failures. With digital wallets now used by 53% of Americans, compliance is more critical than ever.

Key points:

- KYC happens at the start of the customer relationship.

- AML ensures ongoing monitoring of customer behavior.

- Non-compliance can lead to severe penalties, such as fines or loss of banking partnerships.

Quick Comparison:

| Feature | KYC (Know Your Customer) | AML (Anti-Money Laundering) |

|---|---|---|

| Focus | Customer identity verification | Transaction monitoring |

| Timing | During onboarding | Continuous |

| Tools | ID verification, sanctions checks | Transaction tracking, SARs |

| Objective | Prevent identity fraud | Detect financial crimes |

KYC and AML together form a strong compliance framework, helping payment processors maintain trust with banks, regulators, and customers while avoiding legal risks.

::: @figure  {KYC vs AML Compliance: Key Differences for Payment Processors}

{KYC vs AML Compliance: Key Differences for Payment Processors}

KYC & AML Explained What You Need to Know

What is Know Your Customer (KYC)?

KYC is the process of verifying a customer's identity when they open an account. It’s a mandatory step for payment processors to ensure that the individual or business involved in a transaction is genuine and not using a stolen or fake identity.

For payment processors, KYC acts as a safeguard against fraud, identity theft, and money laundering during the onboarding process. Without strong KYC measures, processors risk exposure to fraudulent activities, unauthorized fund transfers, regulatory fines, loss of banking relationships, and even criminal charges for executives.

KYC Definition and Requirements

KYC involves collecting and confirming key customer details to verify their identity. For individual customers, this usually includes:

- Government-issued IDs (e.g., driver’s license, passport)

- Proof of address (utility bills, bank statements)

- Date of birth

- Social Security or tax identification numbers

When onboarding businesses, the process expands into Know Your Business (KYB). KYB requires payment processors to collect:

- Business registration documents

- Proof of the business address

- Information about Ultimate Beneficial Owners (UBOs) - those who own or control at least 25% of the company

- Details of authorized signatories who can legally act on the company’s behalf

This information is then cross-checked against global sanctions lists (like OFAC’s Specially Designated Nationals list), Politically Exposed Persons (PEP) databases, and adverse media sources to identify potential risks. These steps are essential to prevent fraud and ensure compliance with regulations.

Why Payment Processors Need KYC

KYC is critical for payment processors to address key risks during customer onboarding. It prevents synthetic identities, stops account takeovers, and identifies "mule accounts" used to launder money.

In the U.S., strict KYC protocols are legally mandated for Money Services Businesses (MSBs) under the Bank Secrecy Act (BSA) and the USA PATRIOT Act. Failure to comply can result in hefty fines and strained banking relationships, as banks require processors to implement robust measures to keep illicit activities off their platforms.

How the KYC Process Works

The KYC process follows a systematic approach to verify identities and evaluate risks:

- Data Collection: Gathering personal or business information along with supporting documents.

- Identity Verification: Confirming the authenticity of documents and matching them to the applicant. Many processors now use biometric checks, like comparing a selfie to the photo on an ID, to detect spoofing attempts.

- Screening: Cross-referencing customer names with sanctions lists, PEP databases, and adverse media reports.

- Risk Assessment: Assigning either Standard or Enhanced Due Diligence based on transaction risk factors, such as cross-border payments or high transaction volumes. Ongoing reviews ensure compliance beyond the initial checks.

- Record-Keeping: Maintaining documentation of verification steps and decisions for at least five years to meet regulatory requirements. U.S. regulations also require filing Suspicious Activity Reports (SARs) with FinCEN for transactions over $2,000 when fraud or money laundering is suspected [6].

"KYC is more than a compliance requirement; it's a vital tool for protecting businesses from fraud and financial crime while ensuring regulatory compliance."

A solid understanding of KYC is essential for addressing broader financial crime prevention efforts, such as anti-money laundering (AML) measures.

What is Anti-Money Laundering (AML)?

KYC (Know Your Customer) focuses on verifying a customer's identity during onboarding, but AML (Anti-Money Laundering) goes a step further - it ensures ongoing oversight throughout the customer’s relationship with a payment processing platform. AML is a system of laws, processes, and technologies designed to detect, prevent, and report financial crimes like money laundering and terrorist financing [10]. While KYC is a one-time identity check, AML involves continuous monitoring of customer behavior across their account lifecycle [8].

For payment processors, AML compliance is more than just a legal requirement - it’s a critical safeguard against hefty fines and criminal charges. In 2024, North America alone accounted for 95% of global financial penalties tied to AML non-compliance [8].

AML Definition and Purpose

AML frameworks combine regulatory requirements with practical tools to stop criminals from making illegal funds appear legitimate. It focuses on the three stages of money laundering:

- Placement: Depositing illicit funds into the financial system.

- Layering: Moving the funds around to obscure their origins.

- Integration: Reintroducing "cleaned" money into the legitimate economy [11].

Payment processors must align AML programs with global standards like the FATF 40 Recommendations and U.S. laws such as the Bank Secrecy Act (BSA) [10]. These regulations mandate controls like KYC protocols, Customer Due Diligence (CDD), real-time transaction monitoring, and regulatory reporting [8].

"Ensuring compliance with anti money laundering (AML) obligations is not just a legal necessity - it's a foundational element of operational resilience and customer trust."

The stakes for non-compliance are high. In 2023, Binance, a cryptocurrency exchange, faced major enforcement actions from the U.S. Department of the Treasury and FinCEN for failing to maintain an effective AML program [11]. Similarly, an Australian gambling company was fined $450 million AUD for significant AML violations [12].

AML frameworks rely on advanced technologies and strict processes to combat financial crimes effectively.

AML Methods and Technologies

Payment processors use a mix of automated tools and manual oversight to detect suspicious activity. Key technologies include:

- Transaction Monitoring: Automated systems scan activities in real time to flag unusual patterns, such as structuring (splitting large transactions into smaller ones) or sudden spikes in transaction volumes [2].

- Sanctions and PEP Screening: Tools check customers against global watchlists, such as the OFAC Specially Designated Nationals list or UN sanctions databases, and identify Politically Exposed Persons (PEPs) who require extra scrutiny [2].

- AI and Machine Learning: Companies like AML Square support thousands of clients worldwide in maintaining compliance using AI-driven systems. However, new regulations like the EU AI Act are pushing for greater transparency in automated decision-making [9][10].

- Suspicious Activity Reporting (SAR): When unusual behavior is detected, processors must file SARs with authorities like FinCEN (U.S.) or the NCA (UK) without informing the customer [12].

How AML Works for Payment Processors

AML systems ensure continuous monitoring throughout the customer lifecycle, analyzing every transaction to spot potential red flags like layering (disguising illicit origins) or smurfing (breaking large sums into smaller amounts to avoid detection) [11][12]. Modern systems also use velocity checks to identify sudden transaction spikes that could signal criminal activity.

The rise of real-time payments has made AML compliance more challenging. With funds moving instantly rather than in days, AML checks must happen before or during transactions [12]. This is especially critical as digital wallets have become the preferred payment method for 53% of Americans, increasing the volume of data that needs monitoring [3].

Cryptocurrency transactions add another layer of complexity. In 2023, addresses linked to illicit activities transferred approximately $24.2 billion in cryptocurrency [11]. This has forced traditional payment processors to adopt blockchain tracing technologies to mitigate risks from high-risk crypto wallets [12].

"AML compliance program ensures strict AML checks before customers onboarding to minimize this risk [of involvement with high-risk sources]."

- Kushal Jirafe, Compliance Technology Expert, AML Square [10]

Regulatory rules require all AML activities to be documented and retained for at least five years [10][12]. Additionally, payment processors must appoint a Money Laundering Reporting Officer (MLRO) with the authority to escalate issues and make key compliance decisions [12].

KYC vs. AML: Main Differences

KYC (Know Your Customer) and AML (Anti-Money Laundering) play distinct but interconnected roles in a payment processor's compliance strategy. Let’s break down their individual purposes to see how they contribute to managing risk.

KYC focuses on the customer - it’s all about verifying who they are at the start of the relationship[1]. On the other hand, AML is broader and system-focused. It works by continuously monitoring customer transactions, identifying patterns, and cross-checking against global sanctions lists[1].

KYC happens mainly during onboarding, with occasional updates triggered by risk factors or scheduled reviews[1]. AML, however, operates around the clock, analyzing transactions in real time to flag any suspicious activities[1][4]. Given that research shows 70% of fraud occurs after onboarding[13], the importance of constant AML monitoring becomes clear.

Side-by-Side Comparison: KYC vs. AML

| Feature | KYC (Know Your Customer) | AML (Anti-Money Laundering) |

|---|---|---|

| Primary Objective | Verify identity and assess initial risk[1]. | Detect and prevent financial crimes[1]. |

| Scope | Individual/entity verification and identifying ultimate beneficial owners (UBOs)[1][13]. | Monitoring transactions, screening, and reporting suspicious activity[1]. |

| Timing | Conducted during onboarding, with periodic updates or when risks arise[1]. | Ongoing, real-time transaction monitoring[1][4]. |

| Focus | Customer-focused (documents, ID, biometrics)[1]. | System-focused (transaction patterns, sanctions compliance)[1]. |

| Regulatory Tools | ID verification, Customer Due Diligence (CDD), Enhanced Due Diligence (EDD)[1]. | Transaction monitoring, Suspicious Activity Reports (SARs), Politically Exposed Persons (PEP) and sanctions screening[1][13]. |

This table underscores how KYC and AML address different, yet complementary, aspects of compliance.

How KYC and AML Work Together

KYC and AML aren’t standalone processes - they work hand-in-hand to create a layered defense system. KYC lays the groundwork by confirming a customer’s identity and assessing their risk level. This verified data becomes the foundation for AML systems, which use it to monitor transactions and spot unusual behavior in real time[1][4].

Without accurate KYC data, AML systems would struggle to establish what constitutes "normal" behavior for a customer. For payment processors, integrating both frameworks is essential to building a strong risk management system. These distinctions set the stage for understanding the compliance requirements that follow.

Compliance Requirements for Payment Processors

Strict compliance requirements play a critical role in helping payment processors in the U.S. combat financial crime. These regulations ensure that processors adhere to legal standards while protecting the financial system. Below, we'll dive into the key U.S. regulations and the challenges payment processors face when navigating compliance.

U.S. Regulations for KYC and AML

At the heart of anti-money laundering (AML) compliance is the Bank Secrecy Act (BSA). If your business qualifies as a Money Services Business (MSB) under 31 CFR 1010.100(ff), you must register with FinCEN within 180 days of starting operations and renew your registration every two years [5][16].

To meet AML requirements, payment processors need a program that includes:

- Written policies and controls

- A designated BSA/AML Compliance Officer

- Employee training

- Independent audits

- Risk-based Customer Due Diligence (CDD) [5][14][15][16]

Customer Identification Program (CIP) rules (31 CFR 1020.220) require processors to verify key details like name, date of birth, address, and identification number (SSN or ITIN) for individuals. For businesses, processors must collect formation documents and the EIN [15].

Processors must also file Suspicious Activity Reports (SARs) for transactions of $2,000 or more that seem suspicious or lack a lawful purpose. These reports must be submitted within 30 days of detection. In FY2025, MSBs filed 1.26 million SARs, accounting for over 25% of all SARs in the U.S. [5].

"Payment processors... make the payment system vulnerable to money laundering, identity theft, and fraud." - FinCEN [5]

The $3,000 Travel Rule (31 CFR 1010.410) mandates that processors collect and share specific identifying information for fund transfers at or above this amount [5]. Additionally, most states require Money Transmitter Licenses (MTL), each with unique net worth and bonding requirements [16].

Violations of these rules come with steep penalties. For example, Brink's Global Services USA paid a $37 million fine in 2025 for compliance failures [5]. Here’s a breakdown of potential penalties:

| Penalty Type | Maximum Amount |

|---|---|

| Civil Penalties (BSA) | $5,000 per day, per violation [15] |

| OFAC Violations | $1,435,263 per violation (as of 2025) [15] |

| Personal Civil Liability | Up to $100,000 per violation [5] |

| Criminal (Pattern) | $500,000 fine + 10 years imprisonment [5] |

The Office of Foreign Assets Control (OFAC) enforces sanctions compliance, requiring processors to screen transactions against the Specially Designated Nationals (SDN) list [16]. Meanwhile, the Consumer Financial Protection Bureau (CFPB) ensures compliance with Regulation E, which governs unauthorized transactions and error resolution [16].

Looking ahead, a 2026 FinCEN Notice of Proposed Rulemaking (NPRM FINCEN-2026-0034) highlights a shift from "checklist" compliance to evaluating the actual effectiveness of compliance programs [17].

"An 'effective' program is one that is properly established and maintained in all material respects. Examiners will be evaluating whether your controls actually function, not just whether they exist on paper." - Andy Vrabel, Author, Ballerine [17]

Common Compliance Challenges

While regulations provide clear guidelines, implementing them often presents significant hurdles for payment processors. One major challenge is the visibility gap between sponsor banks and end merchants. Sponsor banks often lack direct relationships with merchants, creating opportunities for illicit activities to blend in with legitimate transactions [5]. This issue is especially pronounced in "gateway" or ISO arrangements, where sub-processors resell services to unknown third parties [5][14].

High transaction volumes add another layer of complexity. Manual reviews are nearly impossible at scale, and automated systems become essential. For instance, NACHA requires monitoring thresholds of 0.5% for unauthorized returns and 3% for administrative returns. Exceeding these limits can bring regulatory scrutiny [5].

"Automated systems may be the only realistic method of monitoring transactions." - FATF [5]

Staying updated with regulatory changes is another ongoing challenge. Starting in June 2025, banks and processors can use third-party sources for Taxpayer Identification Number (TIN) verification [15]. Additionally, as of March 21, 2025, U.S. domestic companies are exempt from beneficial ownership reporting under the Corporate Transparency Act, though banks must still verify ownership during account opening [15][18].

Sponsor bank relationships also pose risks. If a processor fails to align with a sponsor bank's compliance program, it can jeopardize the bank's regulatory standing. For example, First Bank of Delaware faced penalties for failing to properly assess the AML risks associated with third-party payment processors and ignoring red flags like high unauthorized return rates [5].

"If your bank sponsor cannot point to how your onboarding decisions, your merchant monitoring, and your escalation workflows contribute to their program's effectiveness, you become a liability in their examination posture." - Andy Vrabel, Author, Ballerine [17]

To address these challenges, many early-stage processors are turning to "Fractional BSA Officers." These experts provide oversight without the cost of a full-time compliance executive, reflecting the growing need for specialized knowledge in an increasingly complex regulatory environment [5].

How to Implement KYC and AML Solutions

To ensure compliance and maintain operational integrity, implementing KYC (Know Your Customer) and AML (Anti-Money Laundering) solutions requires more than just meeting regulatory requirements. It’s about creating systems that are practical and effective. For payment processors, this means building programs that work seamlessly in real-world scenarios. A critical first step is appointing a Money Laundering Reporting Officer (MLRO) who has the authority to escalate issues when necessary [19]. This individual oversees the compliance framework and acts as the primary contact for regulators.

Another key aspect is leveraging Customer Identification Program (CIP) standards for both individual and business accounts [15]. Ideally, verification should be completed before allowing a merchant to process payments, even though FinCEN permits a "reasonable period" for compliance [15]. Modern AI-powered systems can approve over 95% of applications in under 60 seconds, while manual reviews typically take 1 to 3 business days [15].

The following sections explore how to select effective tools, use a risk-based approach, and maintain continuous monitoring.

Choosing Compliance Tools and Software

Technology plays a pivotal role in any compliance program. When selecting tools, focus on integration capabilities - your software should connect effortlessly with your existing onboarding processes through APIs [19]. Automation is essential for scaling operations. For example, AI and machine learning can cut down false positives by up to 88% compared to older screening systems [22].

Your compliance platform should also include global sanctions screening with real-time updates. Some providers refresh risk data every five minutes [22], which is critical given the 6,000+ sanctions introduced globally in 2023 alone [22]. Real-time monitoring can detect unusual patterns like velocity spikes or suspicious routing instantly [19][10]. Additionally, maintain audit-ready logs for at least five years to ensure regulatory compliance [19][10].

The importance of robust compliance tools is highlighted by recent cases. In November 2023, Binance faced a record $4.3 billion fine for inadequate KYC and AML controls - the largest penalty ever imposed on a crypto company [22]. Similarly, daVinci Payments paid over $200,000 in fines for violating sanctions against Cuba, Iran, and Syria [22]. These examples underscore the risks of neglecting proper tools.

Using a Risk-Based Approach (RBA)

A risk-based approach allows you to allocate resources where they are needed most. Customers should be categorized as low, medium, or high risk based on factors like their country of origin, business type, and transaction behavior [20][9].

- Low-risk customers: Typically individuals with small, domestic transaction volumes. Standard KYC verification is sufficient here.

- Medium-risk businesses: Operating in low-risk jurisdictions, these require KYB (Know Your Business) checks and identification of beneficial owners holding 25% or more [22][6].

- High-risk profiles: This includes Politically Exposed Persons (PEPs), high-volume digital wallets, or entities located in FATF grey-list jurisdictions. These cases demand Enhanced Due Diligence (EDD), such as verifying the source of wealth.

"A risk-based approach (RBA) enables payment processors to allocate compliance resources efficiently and in proportion to the level of AML risk."

- Fenergo [8]

For payment processors, monitoring return rates is crucial. High levels of ACH or credit card returns, especially for "insufficient funds" or "unauthorized" transactions, can signal fraud or money laundering risks [14]. Automated triggers should flag these patterns for immediate review, ensuring that your monitoring and escalation processes remain responsive.

Continuous Monitoring and Reporting

Compliance is not a one-time task but an ongoing commitment. Automated systems should continuously monitor transactions for suspicious activities such as sudden spikes in volume, transfers to high-risk regions, or "structuring" (splitting large payments into smaller ones to avoid detection) [8][19]. Daily re-screening of customers against updated sanctions and PEP lists ensures that any status changes are caught promptly [22].

"Truly knowing your customer is not a one-and-done exercise. The details you hold on them need to be as current as possible."

- Rachel Mantock, Remote.com [9]

Annual AML audits are essential for identifying gaps and refining your program [19][10]. Employee training is another critical component - staff involved in onboarding, support, or operations should be equipped to recognize suspicious behavior. Documenting this training is vital for regulatory reviews [19].

In 2024, compliance costs continued to rise, with 99% of financial institutions reporting increases. Across the U.S. and Canada, financial crime compliance costs reached $61 billion [21], emphasizing the growing importance of effective KYC and AML measures.

Conclusion

KYC and AML aren't opposing frameworks - they're complementary. Together, they form the backbone of a solid compliance strategy. While KYC focuses on verifying customer identities and assessing risk during onboarding, AML ensures ongoing transaction monitoring to spot unusual patterns and prevent financial crimes. The two systems are deeply interconnected: without accurate KYC data, AML efforts struggle to distinguish between normal and suspicious activity. On the flip side, KYC alone is just the starting point - it needs AML's continuous oversight to be effective.

For payment processors, integrating KYC and AML is critical - not just for meeting regulatory requirements, but also for maintaining strong banking relationships and securing better payment terms. History has shown that non-compliance can lead to severe penalties, as evidenced by high-profile cases involving major companies. Beyond avoiding fines, a strong compliance framework also strengthens partnerships and improves business valuation. As Ryan Litwin of Borderfree Payments points out, KYC is the first step in verifying identities, while AML ensures ongoing protection through transaction monitoring [4]. This dual approach is especially crucial in industries where transparency and adherence to regulations are non-negotiable.

High-risk sectors like iGaming, cryptocurrency, and fintech face additional hurdles when it comes to compliance, particularly during mergers and acquisitions. In these cases, solid KYC and AML records demonstrate the legitimacy of a customer base, making compliance an asset during negotiations. Platforms like MyReadyMade play a pivotal role in these transactions, offering expert M&A advisory and assistance with license transfers across more than 50 jurisdictions to ensure all compliance needs are met during ownership transitions.

FAQs

Do payment processors need both KYC and AML?

Payment processors usually require both KYC (Know Your Customer) and AML (Anti-Money Laundering) measures to stay compliant and reduce risks. KYC is all about verifying the identities of customers to guard against fraud. On the other hand, AML involves continuous monitoring of transactions to identify and prevent illegal activities. While KYC is a key part of AML, it’s not enough on its own to meet regulatory standards or effectively address financial crimes.

When is Enhanced Due Diligence (EDD) required?

Enhanced Due Diligence (EDD) comes into play when there's a higher risk of money laundering or financial crime. This could involve situations like onboarding clients classified as high-risk, keeping a closer eye on suspicious activities, or tackling additional risks flagged during the initial Know Your Customer (KYC) process.

What triggers a Suspicious Activity Report (SAR)?

A Suspicious Activity Report (SAR) is filed when a financial institution notices transactions or behaviors that could point to money laundering, fraud, or other types of financial crimes. These reports are required when certain criteria or thresholds, as outlined by regulations, are met. SARs play a key role in complying with anti-money laundering (AML) laws, helping to detect and fight against illegal financial activities.

Related Articles

Checklist for Secure Player Database Transfers

Step-by-step checklist for secure player database transfers: compliance, encryption, vendor vetting, zero-trust, integrity checks, and audits.

Ultimate Guide to Payment Compliance in iGaming

Roadmap for building compliant iGaming payment systems: AML/KYC, PCI‑DSS, multi‑PSP setup, chargeback controls and jurisdictional risks.

How Forex Firms Adapt to Regional Preferences

Localize platform features, payments, compliance, and marketing to boost trust and conversions in each Forex market.

Looking to Buy or Sell?

Get in touch with our team for personalized assistance